Humble Group

Ticker: HUMBLE

Humble Group is a Swedish listed FMCG company specializing in delivering healthier and more sustainable FMCG products to consumers globally. The group consists of more than 45 different companies distributing more than 36 thousand products to 12 thousand customers globally.

Humble Group is currently listed on Nasdaq First North Growth with a SEK4.7bn market cap. The company has evolved from an (over-)levered M&A machine into a more reasonable capitalized FMCG company perfectly positioned for the future. Management owns more than 10% of the company and the share currently trades at high single digit FCFE yields while posting double digit organic growth rates.

Disclaimer: I currently own shares in the company.

About the business

Humble Groups was previously listed under the name Bayn Group AB, then a foodtech company focusing on sugar reducing ingredient solutions to the food and beverage industry (mainly) under the brand Eureba.

In 2021 the company bought The Humble Co for apr. SEK800m and changed it name to Humble Group. Since then (starting before the acquisition of the Humble Co to be honest), the group has been growing organically and through M&A - actively acquiring brands that aligned with its mission of bringing sugar-reduced and sustainability focused FMCG products to the market. Over the last 3 years or so the company has made over 40 acquisitions. In 2023 Humble Group made 4 acquisitions, in 2022 they made 13 new acquisitions and in 2021 they completed 23.

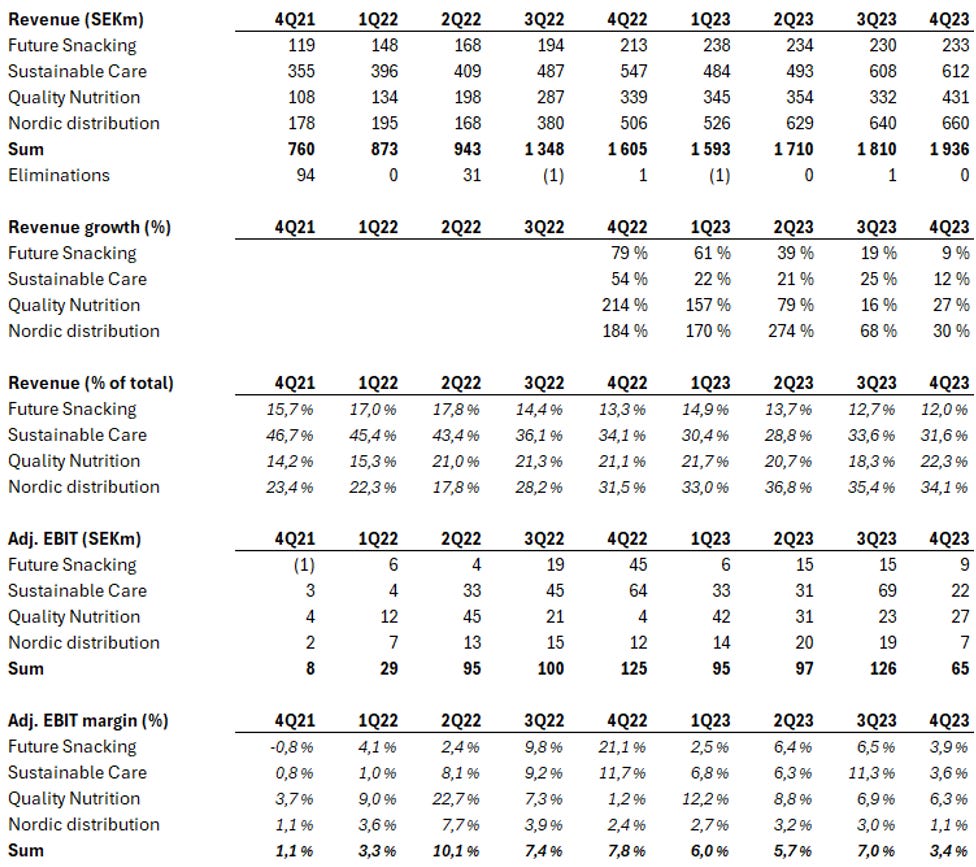

Today, the company reports across 4 distinct business segments which I’ve quickly summarized below.

Future Snacking

Consists of the groups sustainable snacks and assorted eats alternatives, such as TrueGum, Pändy, Tweek and Wellibites. Approximately 13% of the groups’ revenue comes from Future Snacking, which is similar to the segment’s EBIT contribution. From a growth perspective it is the slowest growing segment in the group with an annualized growth rate of approximately 9% as of 4Q24 vs. 20% on an overall level (18% organic).

Sustainable Care

The groups’ offering of organic household, personal care and oral hygiene products that caters to consumers preference for more environmentally friendly alternatives. It includes brands such as The Humble Co., Eco by Naty, The Eco Gang and Delsbo Candle, as well as local distribution companies such as FancyStage (Southern Europe) and Amber House (UK). Additionally, the segment includes what many refers to as the star performer in Humble Group; Solent – a supplier of white label/private label products to consumer product sectors across the UK and in other countries. Worth noting is that Solent is currently being integrated with Go Superfoods, a company which offers similar private label products across a complimentary set of product categories. It will be interesting to see if the combination could be positive from a growth and/or margin perspective. Sustainable Care produces approximately 34% of the groups revenue as of 4Q23, while producing approximately 44% of the Group’s EBIT on a ttm basis. The segment delivers an adjusted EBIT margin of c6% coupled with a rather impressive growth rate of 20% over the last 4 quarters (not adjusted for M&A so probably less on an organic basis).

Quality Nutrition

Quality Nutrition delivers nutritional products, supplements and sports nutrition solutions to consumers and athletes globally. The segment includes several well-known brands such as Body Science (acquired in 2022 and expanded Humbles’ footprint to Australia), Vitargo and Golden Athlete. The historic growth has been solid, but are obviously fueled by the acquisition of Body Science in July 2022. In 4Q23 the segment grew more than 25% on a YoY basis.

Nordic Distribution

Nordic Distribution offers its customers a network of wholesalers and distributors across the Nordic region and aims to be the preferred partners for brands that wants to access the Nordic market. The segment consists of brands such as Privab, Beson, NRG Food and Vital Foods and represents 34% of the groups turnover at SEK2.45bn on a ttm basis as of 4Q23. Given that the segment’s role as a distributor it has rather thin margins. EBIT has been approximately SEK60m over the last year, equating to around 2.5% for the segment.

Below you’ll see how the different segments contribute across the group.

Restructuring the groups’ balance sheet following 3 years of fast-paced inorganic growth

The group’s acquisition spree since 2019 wasn’t fueled by cash flow from operations, which shouldn’t come as a surprise given the way I introduced this post. The historic M&A activities has been realised by a mix of issuance of new shares and debt at somewhat suboptimal terms (if you ask me). Here are a brief overview of Humble’s capital markets activities over the last couple of years:

June 2021: Issues new senior secured bonds of SEK700m under a SEK1.5bn framework.

September 2021: Directed issue of 36m shares raising cSEK845m.

September 2021: Issues subsequent bonds of SEK500m.

April 2022: Announces a directed share issue of approximately SEK530m.

June 2022. Issues bonds under previously established framework totaling SEK250m.

When the company reported its 1Q23 numbers it had 2 senior bonds outstanding. One was a SEK300m senior secured loan at a 9.5% fixed rate issued in January 2021, and the other was a SEK1.5bn bond at STIBOR 3m + 8.25% issued in July of 2021. Needless to say, this led to Humble Group bleeding “profits” down the P&L. In 2Q23 the group’s 12m financial expenses amounted to SEK300m off a 12m adjusted EBITDA base of 586m.

It was at that time quite clear that the company could benefit from restructuring its balance sheet and that it should consider adjusting its capital structure.

About a month or so later that’s exactly what happened. On the 20th of June 2023 the group announced that it had entered into a new credit facilities agreement of SEK1.65bn (+ option to increase it by another SEK300m) and announced a direct share issue raising approximately SEK875m in new equity. The funds was used to refinance the Company’s outstanding bonds of SEK1.8bn and its SEK650m credit facility. As communicated on the Company’s 3rd quarter conference call, approximately SEK1.35bn is now utilized while the SEK300m RCF was not. The new 300 bps margin + STIBOR and an annualized interest costs of approximately SEK30m, leading to annualized savings of approximately SEK130m.

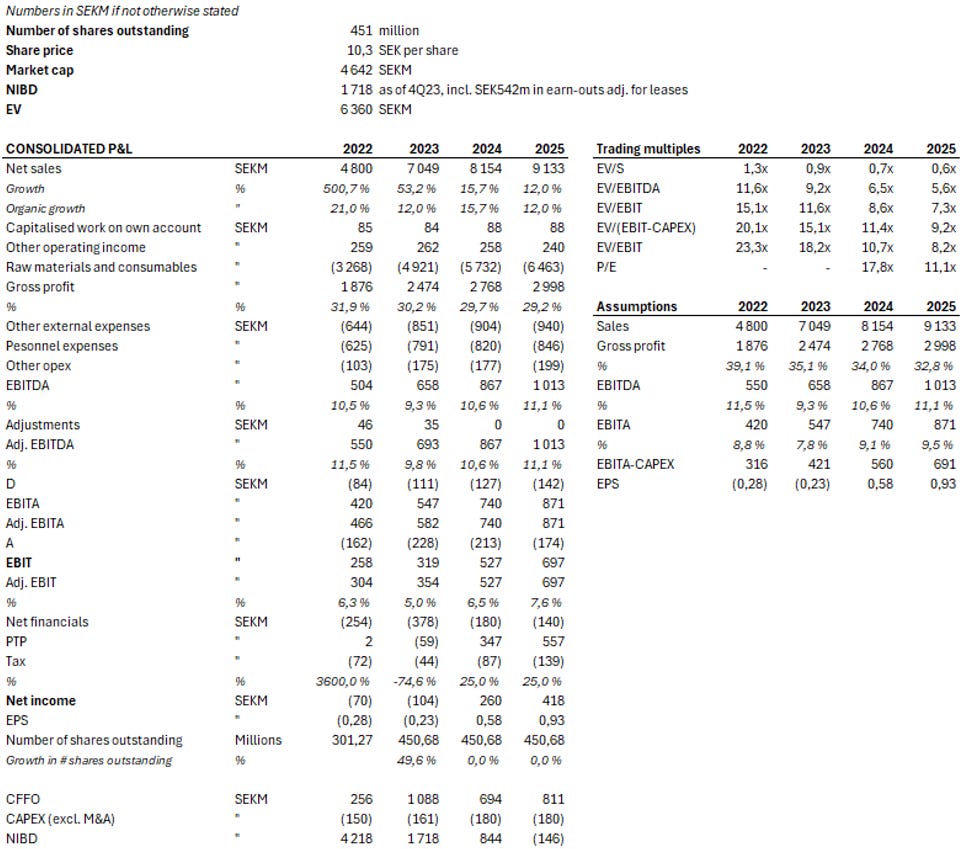

Today the company has approximately SEK1.4bn in NIBD outstanding, a number that includes leasing commitments, but doesn’t reflect earn-outs, recently announced sale-leasback transactions and deferred tax payments. Adjusting for these numbers we’re at SEK1.7bn in NIBD, which is 2.7x trailing 12m adjusted EBITDA and 2.9x reported EBITDA. Earn outs in 2024 as estimated per 4Q23 is approximately SEK350m which will weigh on FCFE as we look into 2024. However, given Humble Group’s CFFO of SEK530 I do believe that’s manageable.

Below are my estimates as they stand today along with trading multiples.

Balance sheet reflections and fair value estimate

Starting with the balance sheet, I must admit that the headline number of close to 3x NIBD/EBITDA is a bit more than what I’d normally be comfortable with. However, on my estimates for 2024 I have Humble generating north of SEK850m in EBITDA and SEK550m in free cash flow after maintenance CAPEX, meaning that I believe the SEK350 in earn out is more than manageable. Thus, I expect a reduction in leverage the next couple of quarters and I am not too worried about the leverage ratio here, also considering the sector the company is in an industry that shouldn’t be partcularly cyclical.

Considering the substantial amount of M&A activity in the past, I do believe (EBITA-CAPEX) is a better number to look at vs. EBIT to set a fair price per share (to account for amortization of amortisation of acquisition-related intangible assets above normalized capex). By that metric, the company is currently trading on a 11.4x multiple, translating into a rough 8.5% FCFF yield assuming a flat WC development over the next year. The CEO believes that WC could come down further in 2024, however I do believe it’s fair to assume that the company needs to build some inventory in order to grow beyond 2024. Taking the 8.8% cash flow yield and the company’s 14%+ organic growth rate (18% in 4Q24) into consideration, I believe investors are compensated well at these levels. I would expect the company to continue taking market share (shelf space) and to grow at least 5-10% rate above inflation for the next handful of years. I also believe that the company will be able to get rid of approximately SEK400m of debt during the next 12 months and that we a year from now will be looking at a business with the ability to generate above SEK690m in free cash flow in 2025. Given that the business will be able to grow high single digits/low double digits organically at an EBITDA margin above 11% (I pencil in 11.1% in 2025) I think that a 15x multiple would be consider fair (even conservative) taking organic growth into consideration. This implies a share price of SEK20, approximately 100% north of where we’re trading at the moment.

Other FMCG peers like Orkla (listed in Norway and also owns several non-FMCG assets) trades at 12.5x EV/EBITA on current 2025 estimates while growing sales at 2.5%. Procter & Gamble trades at 20x growing sales at 3.6%, while Nestle trades at 18x growing sales at 2.4%. Humble Group currently trades at 8.6x – a discount I would argue is too big even considering the company’s smaller scale and inferior balance sheet which I argue should be weighed against Humble growing 4x the rate of its peers.

I would also like to mention that in December 2022 the BoD issued a press statement stating that the company had been in strategic discussions in order to take the company private. The discussions did not result in any public tender offer however. Prior to those discussions the company was trading around a SEK5.8bn Enterprise Value, which at that time equated to apr. 14x EV/EBITA using ttm EBITA numbers. Taking the current NIBD and ttm adj. EBITA numbers into consideration that would corresponds to a share price of approximately SEK15/sh.

CEO and management

The group’s current CEO Simon Petrén is one of the company’s largest owners (directly and indirectly via his network). Simon joined Humble Group from Pändy, a company acquired by Bayn in 2019. Simon was part of Pändys founding team back in 2016 and is quite young (born in 1989) compared to most CEOs of publicly listed companies. In fact, no one in the current management team is born prior to 1988, which I must admit is quite extraordinary for a publicly listed company. Hopefully they all have a long-term mindset when it comes to developing Humble Group, and I must say that 2024 will be an important year for them the way I see it. I will definitely be looking for them to prove that they’ll be able to transition from a group focused on growth and M&A, towards a group with a greater emphasis on profitable growth and M&A funded by organic cash flows. I also want to highlight Humble Groups current VP/COO Noel Abdayem, who also is a large shareholder and who has an impressive background and solid track record having built The Humble Co from the ground up.

Summary

To conclude, I believe that Humble Group offers investors an attractive entry into a fast-growing FMCG company well positioned to meet a growing crowd of health and environment conscious consumers globally. Management has significant skin in the game with Simon and his family owning approximately 4.2% of the company, and should have a lot of incentives to create shareholder value long-term. At around SEK10-11/sh, Humble Group trades at high single digit (8%+) free cash flow yields on 2024E numbers while being positioned to deliver low double digit organic growth rates for years to come. Moreover, I believe the company might offer strategic value to larger players in the spacer and that the group as such should be considered an acquisition target for both private equity and larger FMCG companies.

I believe the company will focus on delivering its balance sheet going into the first half of 2024 through continued focus on improving gross margins and working to further optimize working capital. If that happens, I believe M&A will be back on the table going into 2H. However, judging by the CEO’s remarks on the conference call for 4Q24 I would expect (and certainly hope) that those transactions would be largely funded by internal cash flows and (smaller) use of the company’s RCF - hopefully with a strict focus healthy on cash ROIC and IRRs to drive value per share for its owners (as opposed to multiple arbitrage driven M&A).

Current owners includes RoosGruppen with 46m shares, Neudi & Co with c45m shares, as well as Simon Petrén and his family with apr. 19m shares and Noeal Abdayem (founder of The Humble Co) who holds 27m shares. Lastly, and notably from my perspective, Alta Fox Capital currently owns 26m shares in the company. I must admit that I admire what Connor has been able to achieve ever since he started Alta Fox in late 2017 and I find it very positive to see them on the cap table he.

Sources/references

Humble Group Investor Relations – Various Annual and Quarterly Reports, incl. recordings and company filings

Småbolagspodden – 25. Humble Group – 500 miljoner till förvärv

Alta Fox Capital Research – Humble Group AB – Cheapest Consumer Staples Company in the World

Hi Only. Currently working on a review/update, so I'll let you know. TLDR; No, but I have reasonable hopes of fundamentals turning from here. Still too cheap imo.

Do you still like Humble Group? Has the company performed as you hoped?